Change of volatility

August 5, 2020, 8:19 AM

Indicators

0 Comments

{kind=link}

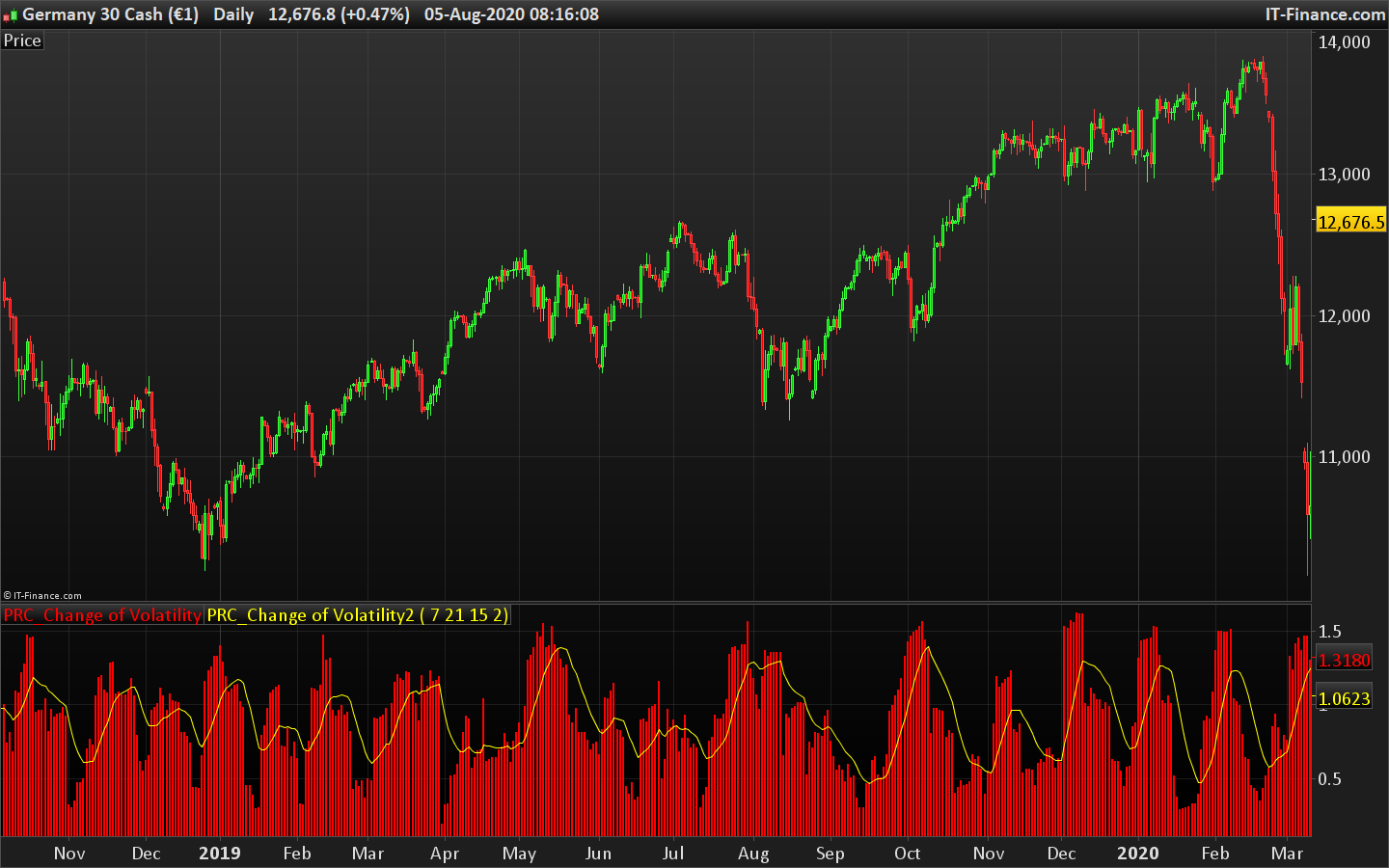

There are a lot of ways to measure volatility (changeability). One of them is calculation of the standard deviation of returns for a certain period of time. Sometimes the current volatility on a short period of time (for example, 6 days) is correlated with volatility of a larger period (for example 100 days). This indicator calculates the correlation of a short volatility Vol_short and a long volatilityVol_long. Vol_change=Vol_short/Vol_long

Standard deviation here is not that from a difference of closing prices, but from logarithms of the correlation of the current day closing price and closing price of a previous day: Mom[i]=Close[i]/Close[i+1].

Vol_k=Std(Mom,k),

where k is the period of volatility change.

(description from the author)

Indicator of volatility converted following a request in the indicators forum section.

//PRC_Change of Volatility | indicator

//05.08.2020

//Nicolas @ www.prorealcode.com

//Sharing ProRealTime knowledge

//converted from MT4

//https://www.prorealcode.com/topic/conversion-of-indicator-change-of-volatility-from-mt4/

// --- settings

Short = 6

Long = 100

SigMA = 15

SigMAMode = 2 //0 = SMA 1 = EMA 2 = WMA 3 = Wilder 4 = Triangular 5 = End point 6 = Time series 7 = Hull (PRT v11 only) 8 = ZeroLag (PRT v11 only)

// --- end of settings

Moment=Momentum[1](close)/100

HVBuffer=std[Short](Moment)/std[Long](Moment)

Ma = average[SigMA,SigMAMode](HVBuffer)

return HVBuffer coloured(255,0,0) style(histogram), Ma coloured(255,255,0) style(line,1)

Download

Filename:

PRC_Change-of-Volatility.itf

Downloads:

170

Master

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...