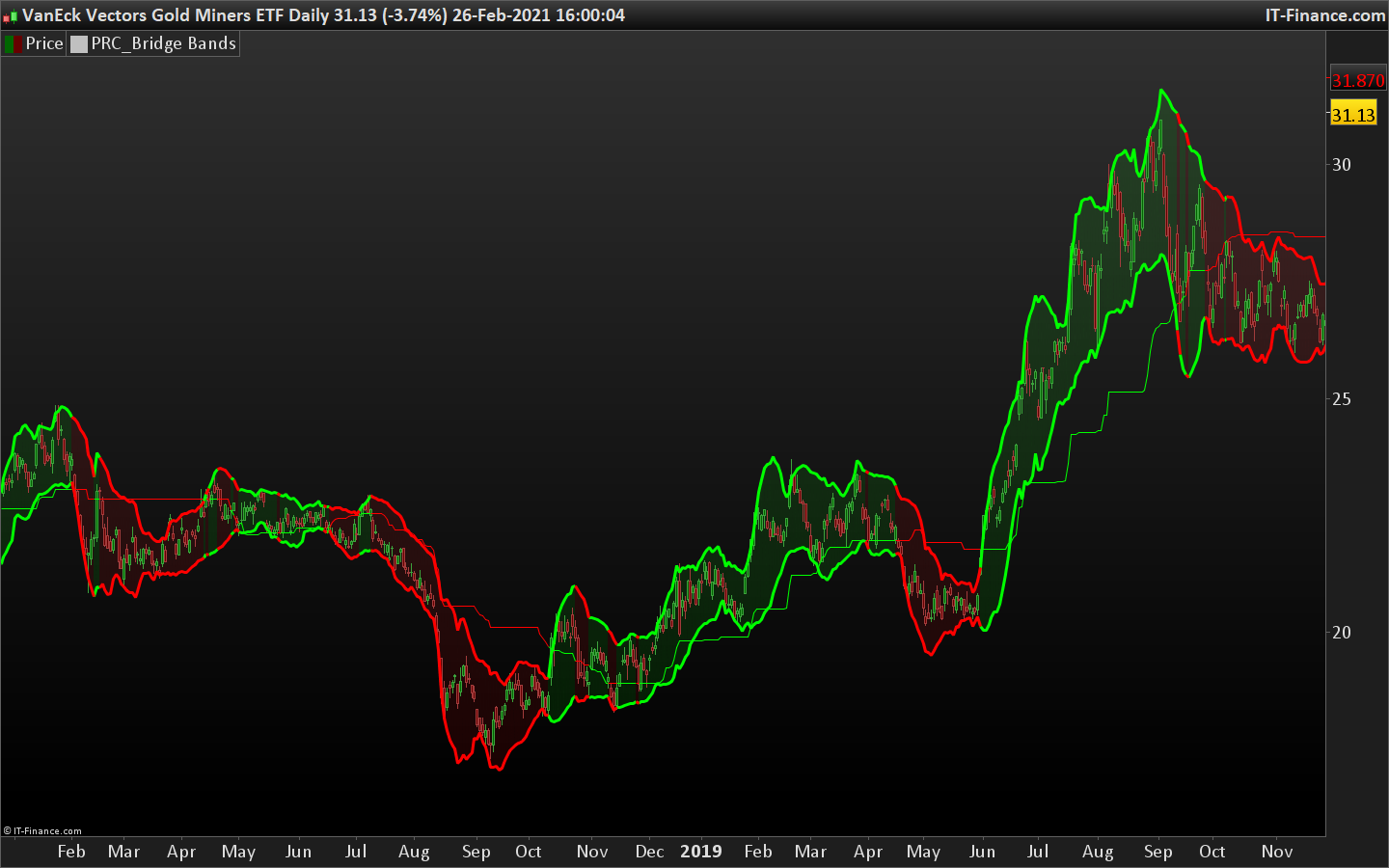

Bridge Bands

March 1, 2021, 10:51 AM

Indicators

10 Comments

{kind=link}

Bridge Bands are an implementation of the work done by Joe Catanzaro (joecat808) to produce a risk range for a security.

The basic idea is to calculate Mandelbrot’s “Bridge Range”. ( Pg . 179 of Misbehavior of Markets)

It then calculates Bollinger Bands .

Then next step is to calculate the Hurst Exponent .

The last step is to merge the Bridge Range and the Bollinger Bands . The basic concept is if H = .5 we use the Bollinger Bands and the farther away we move from .5 in either direction the Bridge Range takes more precedent.

There is a Trend value that is the mid-point of a 3 month Donchian Channel. If price is above we’re bullish , if price is below we’re bearish.

(description of original author: calebsandfort)

//PRC_Bridge Bands | indicator

//01.03.2021

//Nicolas @ www.prorealcode.com

//Sharing ProRealTime knowledge

// --- settings

length = 15 //Length

trendLength = 63 //Trend Length

resolution = 0 //Resolution

//topRiskRangePositionSizePtg = 25 //Top RR Position Size %

//midRiskRangePositionSizePtg = 75 //Mid RR Position Size %

//bottomRiskRangePositionSizePtg = 125 //Bottom RR Position Size %

// --- end of settings

//topRiskRangePositionSizePtg = topRiskRangePositionSizePtg/100

//midRiskRangePositionSizePtg = midRiskRangePositionSizePtg/100

//bottomRiskRangePositionSizePtg = bottomRiskRangePositionSizePtg/100

timeframe(daily,updateonclose)

securityclose = close[resolution]

securityhigh = high[resolution]

securitylow = low[resolution]

lengthMinus1 = length - 1

slope = (securityclose[0] - securityclose[lengthMinus1]) / lengthMinus1

//min diff

m = 100000000.0

for i = 0 to lengthMinus1

m = min(m, securityclose[lengthMinus1 - i] - (securityclose[lengthMinus1] + (slope[0] * i)))

next

mindiff=m

//max diff

m = -100000000.0

for i = 0 to lengthMinus1

m = max(m, securityclose[lengthMinus1 - i] - (securityclose[lengthMinus1] + (slope[0] * i)))

next

maxdiff=m

bridgerangebottom = securityclose + mindiff

bridgerangetop = securityclose + maxdiff

ATR = AverageTrueRange[length](close)

logLength = log(length)

hurst = (log(highest[length](securityhigh) - lowest[length](securitylow)) - log(ATR)) / logLength

sd = std[length](securityclose)

WMA = WeightedAverage[length](securityclose)

bbbottom = WMA - (sd * 2)

bbtop = WMA + (sd * 2)

bridgebandbottom = bbbottom + ((bridgerangebottom - bbbottom) * abs((hurst * 2) - 1))

bridgebandtop = bbtop - ((bbtop - bridgerangetop) * abs((hurst * 2) - 1))

bridgebandmid = bridgebandbottom + ((bridgebandtop - bridgebandbottom) / 2)

trend = lowest[trendlength](securitylow) + ((highest[trendlength](securityhigh) - lowest[trendlength](securitylow)) / 2)

bullish = securityclose > trend

if bullish then

r=0

g=255

else

r=255

g=0

endif

timeframe(default)

//Band Fills

drawtriangle(barindex[1],bridgebandtop[1],barindex,bridgebandbottom,barindex[0],bridgebandtop[0]) coloured(r,g,0,25) bordercolor(r,g,0,0)

drawtriangle(barindex[1],bridgebandtop[1],barindex[1],bridgebandbottom[1],barindex[0],bridgebandbottom[0]) coloured(r,g,0,25) bordercolor(r,g,0,0)

return trend coloured(r,g,0),bridgebandbottom coloured(r,g,0) style(line,3),bridgebandtop coloured(r,g,0) style(line,3)

Download

Filename:

PRC_Bridge-Bands-1.itf

Downloads:

227

Master

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...