Adaptive CCI

March 3, 2016, 3:31 PM

Indicators

4 Comments

{kind=link}

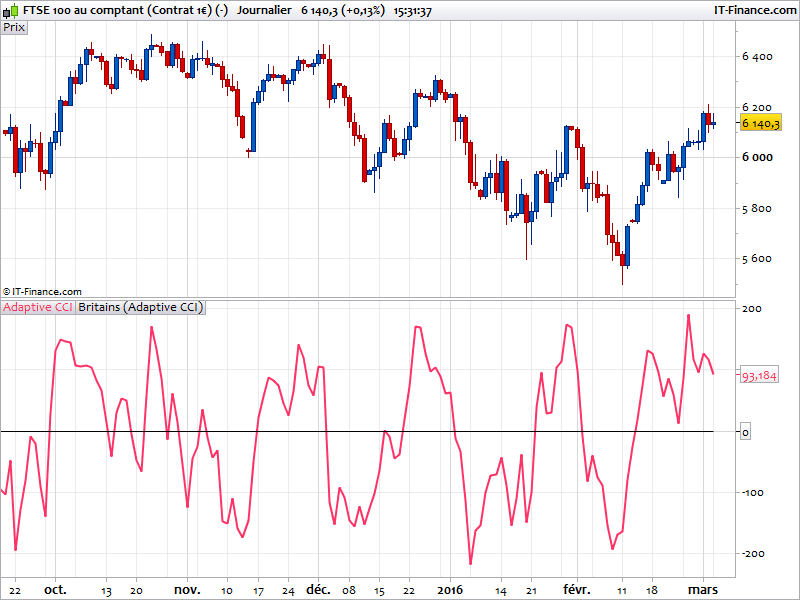

This is the Ehlers’ adaptive CCI code. The modified John Ehlers version of the CCI adapt the classical CCI period dynamically adapted to the market cycle. It tends to give more better indication as the CCI indicator itself.

c = 0.5

pri=Customclose

CycPart=c

If Barindex > 5 Then

Smooth=(4*pri+3*pri[1]+2*pri[2]+pri[3])/10

Detrender=(0.0962*Smooth+0.5769*Smooth[2]-0.5769*Smooth[4]-0.0962*Smooth[6])*(0.075*Period[1]+0.54)

REM Compute InPhase & Quadrature Components

Q1=(0.0962*Detrender+0.5769*Detrender[2]-0.5769*Detrender[4]-0.0962*Detrender[6])*(0.075*Period[1]+0.54)

I1=Detrender[3]

REM Advance The Phase Of I1 & Q1 By 90 Degrees

jI=(0.0962*I1+0.5769*I1[2]-0.5769*I1[4]-0.0962*I1[6])*(0.075*Period[1]+0.54)

jQ=(0.0962*Q1+0.5769*Q1[2]-0.5769*Q1[4]-0.0962*Q1[6])*(0.075*Period[1]+0.54)

REM Phasor Addition

I2=I1-jQ

Q2=Q1+jI

REM Smooth The I & Q Components

I2=0.2*I2+0.8*I2[1]

Q2=0.2*Q2+0.8*Q2[1]

REM Homodyne Discriminator

Re=I2*I2[1]+Q2*Q2[1]

Im=I2*Q2[1]-Q2*I2[1]

Re=0.2*Re+0.8*Re[1]

Im=0.2*Im+0.8*Im[1]

If Im <> 0 And Re <> 0 Then

Period=360/ATAN(Im/Re)

Endif

If Period > 1.5*Period[1] Then

Period=1.5*Period[1]

Endif

If Period < 0.67*Period[1] Then

Period=0.67*Period[1]

Endif

If Period < 6 Then

Period=6

Endif

If Period > 50 Then

Period=50

Endif

Period=0.2*Period+0.8*Period[1]

SmoothPeriod=0.33*Period+0.67*SmoothPeriod[1]

Length=Round(CycPart*Period)

MP=(High+Low+Close)/3

Avg=0

For count=0 To Length-1

Avg=Avg+MP[count]

Next

Avg=Avg/Length

MD=0

For count=0 To Length-1

MD=MD+ABS(MP[count]-Avg)

Next

MD=MD/Length

If MD <> 0 Then

ACCI=(MP-Avg)/(0.015*MD)

Endif

Endif

Return ACCI as "Adaptive CCI",0

//indicator from the Kevin Britains archive.

Download

Filename:

Britains-Adaptive-CCI.itf

Downloads:

263

Legend

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...