Partial closure of positions when price is retracing – A complete function

Now that multi-timeframe support is available for ProOrder, there are many new possibilities for us, including position management in a more refined and faster way than before.

Indeed, it is now possible to trade a strategy that makes trading decisions in a timeframe different from the one we will use to manage its positions.

In this article, I’m going to expose a rather simple function of partial closure of position when the price retraces to your disadvantage.

To close or not to close? That is the question!

Entering position is easy! But how to get out? It is often much more difficult to manage a position exit than to find the best way to enter it.

Should we close on a contrary signal? On a support or a resistance? Or through a thousand other arithmetic tests based on empirical statistics? Hard to say. In fact there would be only one good way, it is based on the behavior of the price, it is the purpose of the function below.

Partially close your position when the price is continuously retracing

The idea of the function is simple:

If the price was in profit of X points, then one starts the function of partial closure. At this point, if the price retrace Y points from the highest price (for a long order), then we close Z percent of the remaining position. The highest price reached is then reset to the current price. And so on until exhaustion of the position (its total closure).

That’s the function code, which incorporates a simple SuperTrend indicator-based strategy on a 15-minutes timeframe:

defparam cumulateorders=false

// --- Partial Close settings ---

size = 10

mincontracts = 1

trigger = 20

pointback = 5

closepercent = 20

// ------------------------------

timeframe(15 minutes,updateonclose)

st = Supertrend[3,10]

if not longonmarket and close crosses over st then

buy size contracts at market

set stop ploss 15

endif

if not shortonmarket and close crosses under st then

sellshort size contracts at market

set stop ploss 15

endif

timeframe(1 minute)

if not onmarket then

AllowPartialClose=0

endif

//## -- PARTIAL CLOSE PRICE BACK FUNCTION -- ##

//## - BUY ORDERS

if longonmarket then

//trigger for the partial closure function to start

if close-tradeprice>=trigger*pointsize then

AllowPartialClose = 1

endif

if AllowPartialClose then

//compute the maxprice reached

maxprice = max(maxprice,close)

//check to trigger a partial closure or not

if maxprice-close>=pointback*pointsize then

//close partially

sell max(mincontracts,size*(closepercent/100)) contracts at market

//reset the maxprice to the current price

maxprice = close

endif

endif

endif

//## - SELLSHORT ORDERS

if shortonmarket then

//trigger for the partial closure function to start

if tradeprice-close>=trigger*pointsize then

AllowPartialClose = 1

endif

if AllowPartialClose then

//compute the maxprice reached

minprice = min(minprice,close)

//check to trigger a partial closure or not

if close-minprice>=pointback*pointsize then

//close partially

exitshort max(mincontracts,size*(closepercent/100)) contracts at market

//reset the maxprice to the current price

minprice = close

endif

endif

endif

graph st coloured(200,100,200) as "Supertrend"

graph CloseThe parameters are as follows:

- size = 10

Size of the initial position opened by the strategy.

- mincontracts = 1

Minimum contract size to close (corresponds to the minimum size possible for the instrument), so to set according to the instrument on which you will perform this function.

- trigger = 20

From how many points of profit the function will start

- pointback = 5

Step to close a position, in points, since the highest price (BUY) or lowest (SELLSHORT) ever reached

- closepercent = 20

Closure size at each level, in this example, 20% of “size” = 10*0.2 = 2 contracts

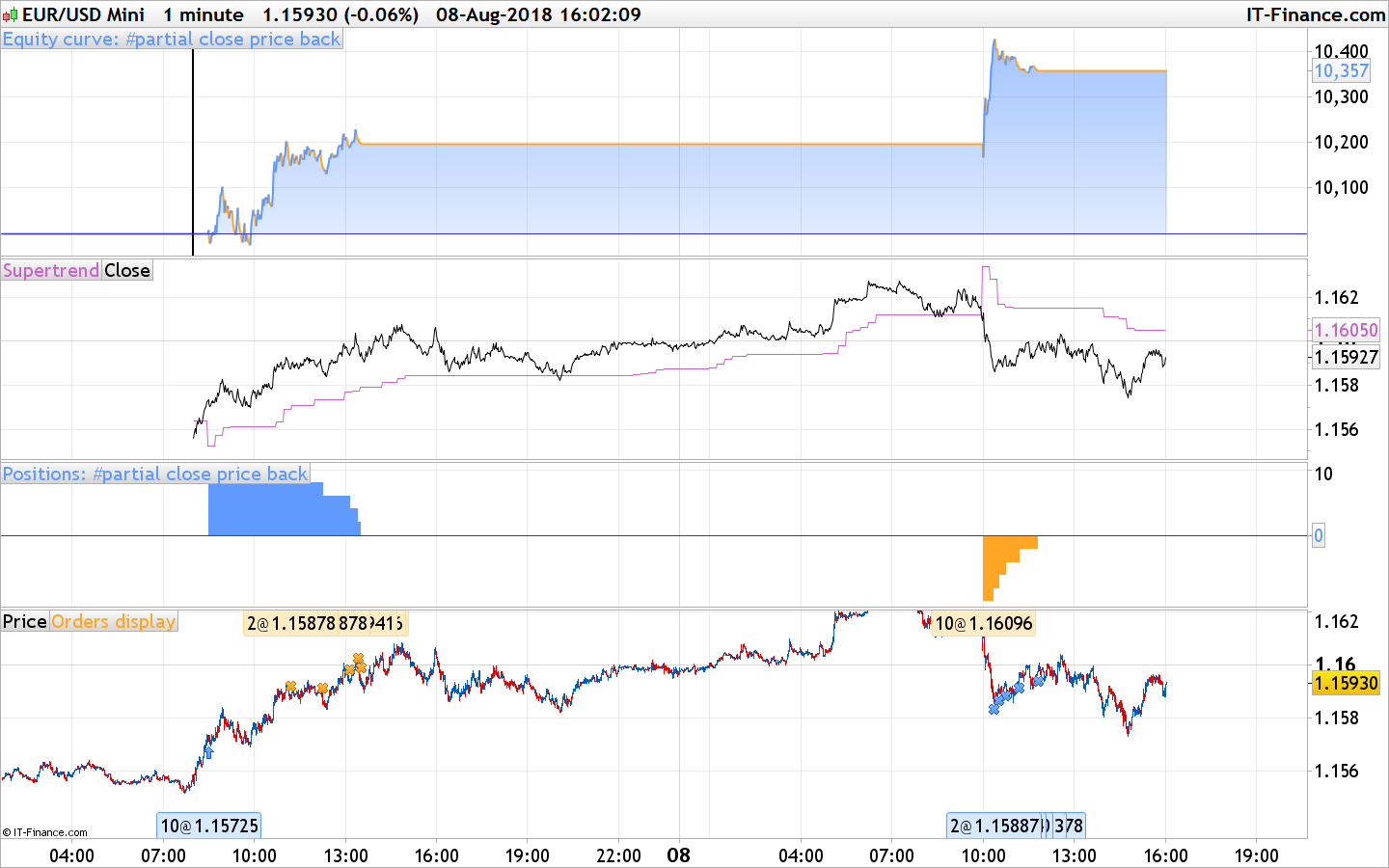

Buy position – partial closure:

Extend the function with many other ideas!

Many ideas could be added to this way of managing closures, for example:

- allow closures only if the price is above / below a moving average or any other indicator,

- no longer allow partial closure if the order is already at breakeven,

- change the closing size at each step,

- achieve a dynamic closure stage based on other analyzes,

- etc.