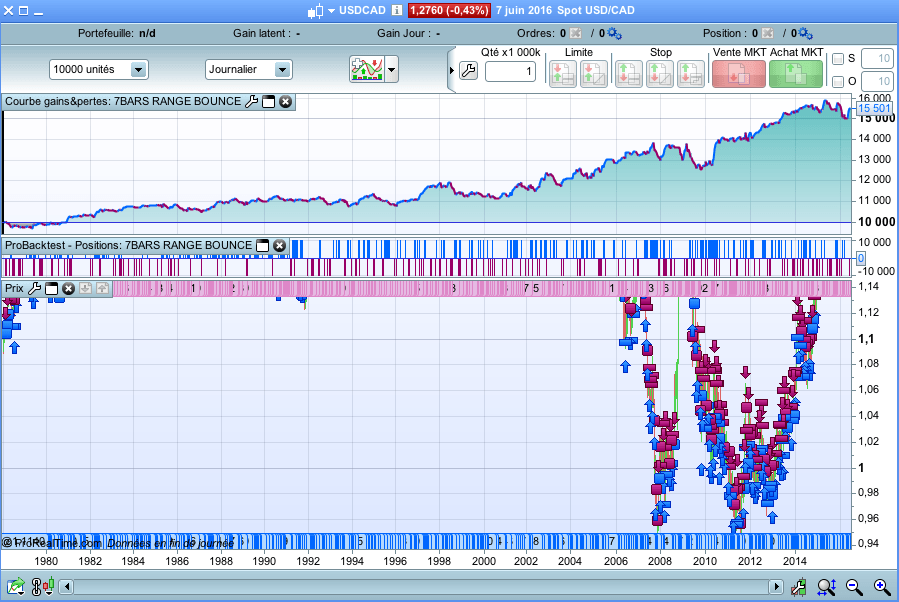

The "7 Bars" Range Bounce

{kind=link}

Hello everyone,

Here’s a little strategy of my own. Actually, I wanted to test the breakout of a range defined by a number of candles, and I’ve realized that the rebound was more profitable.

How does the strategy work ?

We consider a bar signal if its amplitude (high – low) is less than the amplitude of each of the previous 6 bars. In this case, we place two orders :

- “buy limit” at the lowest of the last 6 previous candles

- “sell limit” at the highest of the last 6 candles.

This means that we play the bounces between the high and the low of the range.

The take profit is set at the middle the range, the stop loss is equal to the take profit.

By changing the parameters, you could have a backtest with a “perfect” equity curve.

It nearly always mean that the stop loss and take profit are often on the same candle, and in this case the backtest record only the take profit. I hope ProRealTime will soon fix this issue.

But for these parameters, it seems to work well.

Defparam cumulateorders = false

n = 10

RANGE7 = high - low < high[1] - low[1] and high - low < high[2] - low[2] and high - low < high[3] - low[3] and high - low < high[4] - low[4] and high - low < high[5] - low[5] and high - low < high[6] - low[6]

IF RANGE7 THEN

HAUT = highest[6](high)

BAS = lowest[6](low)

amplitude = haut - bas

buy n shares at BAS limit

sellshort n shares at HAUT limit

ENDIF

set stop loss amplitude/2

set target profit amplitude/2