HighLow Adaptive Momentum Cycle

August 28, 2016, 7:10 AM

Indicators

16 Comments

{kind=link}

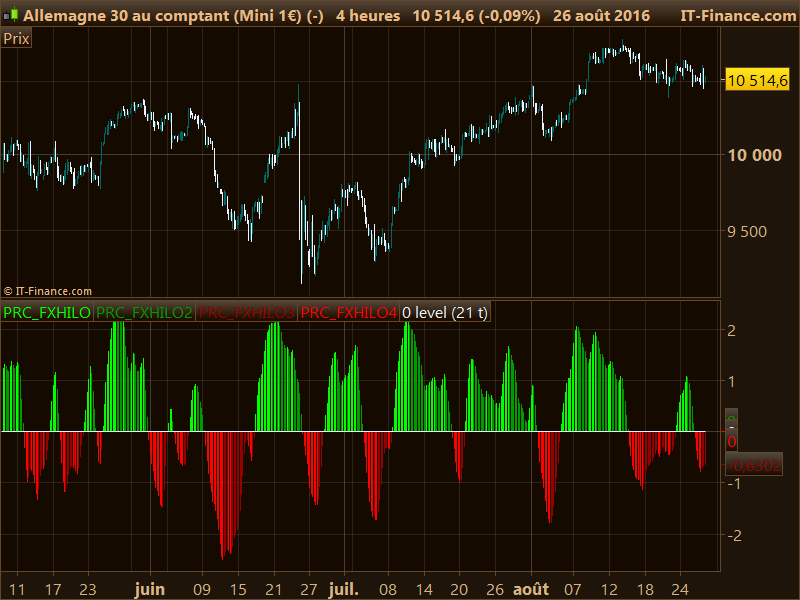

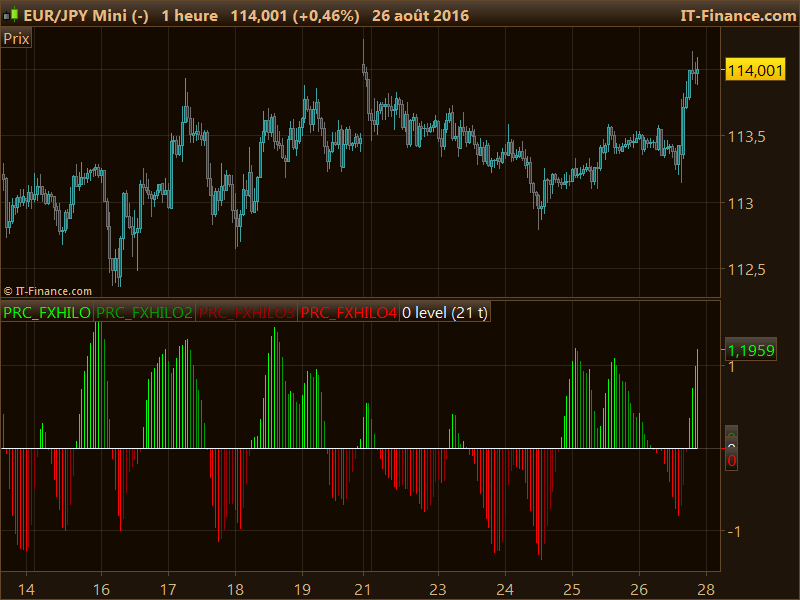

Here is a new oscillator made of a cycle calculation of the median price calculated from the highest high and lowest low of the last x periods.

An adaptive period formula can be activated to calculate the “best” period of the hi/lo channel because of market noises.

I added 4 different returned buffers to identify when the oscillator is increasing or declining above of below the 0 level which represent the bull/bear side of the market.

// parameters

// myPeriod = 21

// Adaptive = 1 //boolean

once f = 0

once g = 0

if barindex>myPeriod then

//adaptive period

averagePeriod = myPeriod

if adaptive=1 and averagePeriod > 1 then

price = medianprice

minPeriod = round(averagePeriod/2.0)

maxPeriod = minPeriod*5.0

endPeriod = round(maxPeriod)

signal = Abs((price-stored[endPeriod]))

noise = 0.00000000001

for k=1 to endPeriod do

noise=noise+Abs(price-stored[k])

averagePeriod = round(((signal/noise)*(maxPeriod-minPeriod))+minPeriod)

next

endif

stored=price

averageperiod=max(averageperiod,2)

myHigh = Highest[abs(averagePeriod)](high)

myLow = Lowest[abs(averagePeriod)](Low)

mean = (High + Low) / 2.0

myVAR1 = 0.66 * ((mean - myLow) / (myHigh - myLow) - 0.5) + 0.67 * f

myVAR1 = Min(Max(myVAR1, -0.999), 0.999)

fxhilo = Log((myVAR1 + 1.0) / (1 - myVAR1)) / 2.0 + g / 2.0 //main line

f = myVAR1

g = fxhilo

if fxhilo>fxhilo[1] and fxhilo>0 then

plusone = fxhilo

plustwo = 0

minusone = 0

minustwo = 0

elsif fxhilo<fxhilo[1] and fxhilo>0 then

plusone = 0

plustwo = fxhilo

minusone = 0

minustwo = 0

elsif fxhilo>fxhilo[1] and fxhilo<0 then

plusone = 0

plustwo = 0

minusone = fxhilo

minustwo =0

elsif fxhilo<fxhilo[1] and fxhilo<0 then

plusone = 0

plustwo = 0

minusone = 0

minustwo = fxhilo

endif

endif

RETURN plusone coloured(0,255,0), plustwo coloured(0,155,0), minusone coloured(150,0,0), minustwo coloured(255,0,0), 0 as "0 level"

Download

{kind=link}

Filename:

momentum-adaptive-cycle.png

Downloads:

85

Download

Filename:

PRC_FXHILO.itf

Downloads:

177

Master

Trader, Programmer, Coder enthusiast. Work with each other for a common goal.

Author’s Profile

Comments

Loading...