"RSI-2 Strategy" from Larry Connors

April 1, 2016, 2:20 PM

Strategies

11 Comments

{kind=link}

Hi all !

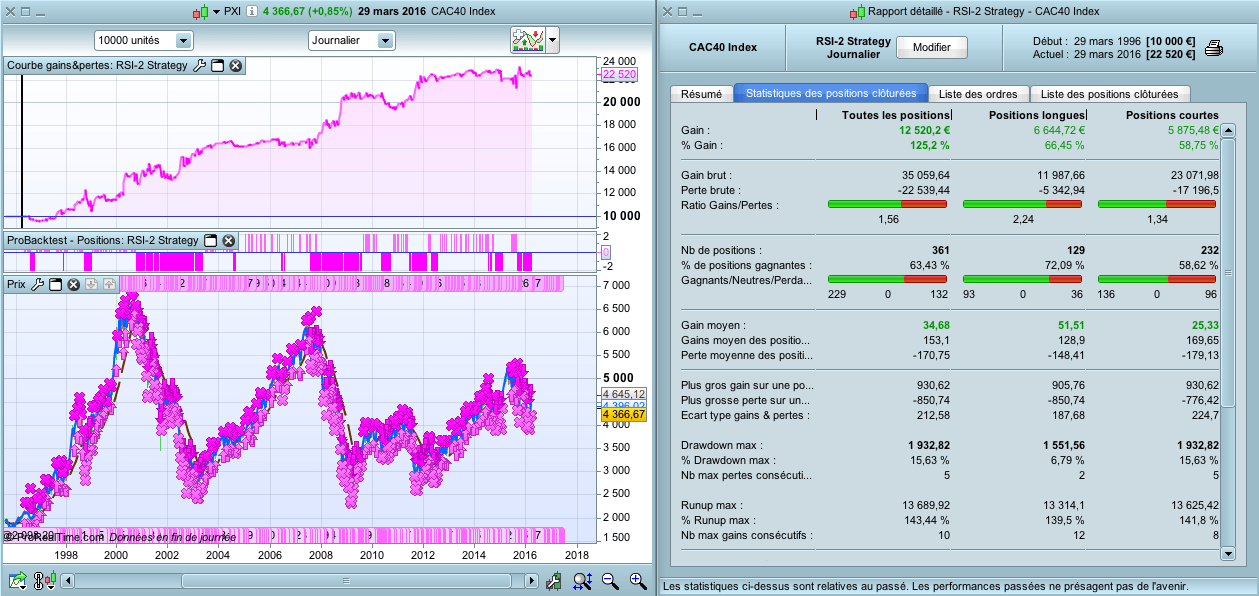

Here is the backtest that I made, from the « RSI-2 Strategy » of Larry Connors.

He’s also the co-author of the « Cumulative RSI » Strategy.

It took me 5 minutes to write the code, as the rules are very simple : no need to detail them.

Even if the strategy is positive on many stocks, indices, I don’t find it that great.

But you are free to test it and why not improve it.

The picture shows the CAC40 for the last 20 years.

Best Regards,

DEFPARAM CumulateOrders = False

n = 2

// Conditions pour ouvrir une position acheteuse

MM200 = Average[200](close)

MM5 = Average[5](close)

RSI2 = RSI[2](close)

c1 = close > MM200

c2 = close < MM5

c3 = RSI2 < 10

IF c1 AND c2 AND c3 THEN

BUY n SHARES AT MARKET

ENDIF

// Conditions pour fermer une position acheteuse

c4 = close > MM5

IF c4 THEN

SELL AT MARKET

ENDIF

// Conditions pour ouvrir une position en vente à découvert

c1v = close < MM200

c2v = close > MM5

c3v = RSI2 > 90

IF c1v AND c2v AND c3v THEN

SELLSHORT n SHARES AT MARKET

ENDIF

// Conditions pour fermer une position en vente à découvert

c4v = close < MM5

IF c4v THEN

EXITSHORT AT MARKET

ENDIF

Download

Filename:

RSI2-Strategy.itf

Downloads:

638

Master

Hello, I'm Marc.

Nice to meet you.

Author’s Profile

Loading...