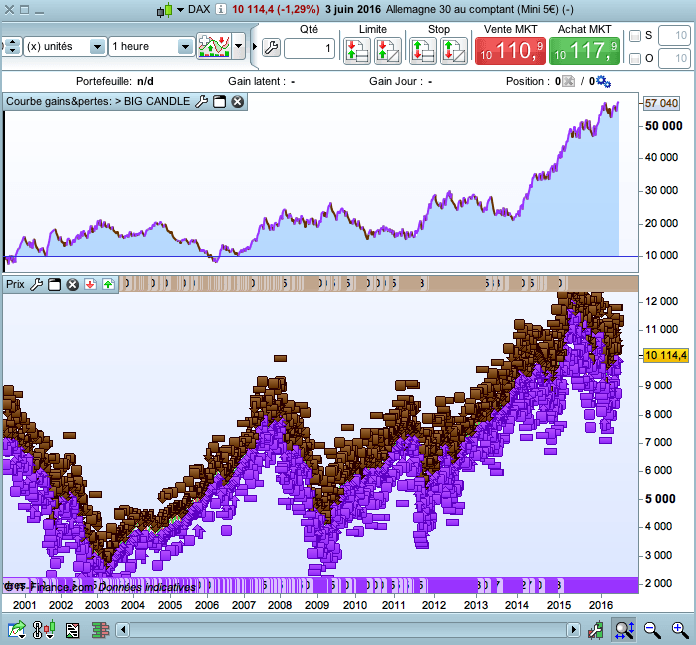

The "BIG Candle" strategy

June 6, 2016, 8:20 AM

Strategies

2 Comments

{kind=link}

Hi all,

This strategy can be applied on any timeframe.

It seems to be very very profitable on M15 timeframe on the DAX. But because of the spread, it’s not really winning.

So you must test it on > H1 timeframe.

The strategy takes position with a “big candle”, which breaks the highest(8) or lowest(8), and with an amplitude > ATR(24).

The take profit is same to the stop loss * 1.5

The backtest is made with 1 point spread on the DAX (trades taken from 09AM to 5PM).

Maybe someone could improve it.

Best regards,

DEFPARAM CumulateOrders = False

n = 1

Haut = highest[8](high[1])

Bas = lowest[8](low[1])

amplitude = abs(close - open)

Ctime = time >= 090000 and time <= 170000

// CONDITIONS ACHAT

c1a = close > open

c2a = close > Haut

c3a = amplitude > AverageTrueRange[24]

IF c1a AND c2a AND c3a AND Ctime THEN

BUY n shares AT MARKET

ENDIF

// CONDITIONS VENTE

c1v = close < open

c2v = close < Bas

c3v = amplitude > AverageTrueRange[24]

IF c1v AND c2v AND c3v AND Ctime THEN

sellshort n shares AT MARKET

ENDIF

// STOP LOSS & TAKE PROFIT

sl = 20 // 20 en M15 75 en H1

set stop loss sl

set target profit sl*2

Download

Filename:

BIG-CANDLE.itf

Downloads:

171

Master

Hello, I'm Marc.

Nice to meet you.

Author’s Profile

Loading...