ALEX AutoTradingBot INDEX

{kind=link}

This strategy was explained at The Forex Day in Madrid by Lex Smirnoff in 2015. I’m Adolfo so, A-LEX will be a beautiful name for it! :-). Is explained to trade it in GBP/USD in 1 hour chart.

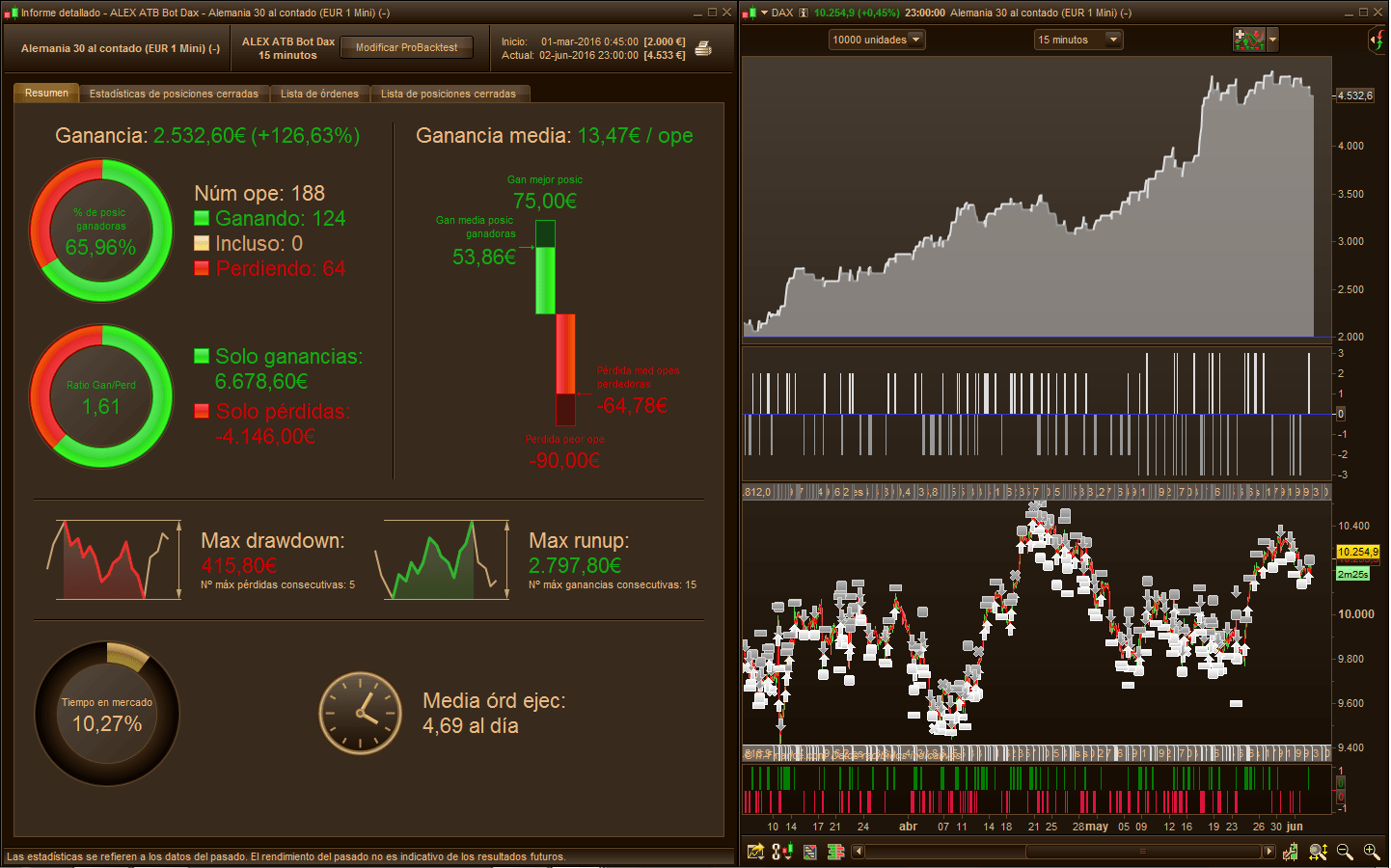

Since I <3 indexes like DAX or DOW couln’d wait to test it. Since March I’m doing discretionary trading on both markets in a real account, with profitable results (38,12%), first trades were made with 7% risk per trade, but I’ll no longer recommend it for you or anyone, it’s crazy!

A lot of entrance were missed by my fault, just wondering about if it’s a good moment or not…. will keep rising? or not? Low confidence took me here, and finally I can share it with you, is already automated. Enjoy it!

Requirements

.ITF file: ALEX ATB Indicator Signal (Click and get it)

Indicator code:

REM Variables

mm = Exponentialaverage[8](close)

once uma=Highest[8](high)

once umb=Lowest[8](low)

objetivo=45*pipsize

if High > mm and Low < mm then // TOuching Ema8

tb = BarIndex

ltp = mm

uma = mm

umb = mm

endif

if low>mm then // New bullsih movement

n = BarIndex - tb

uma=Highest[n](high)

umb=mm

endif

if high<mm then // New bearish movement

m = BarIndex - tb

umb=Lowest[m](low)

uma=mm

endif

if (uma-ltp)>objetivo and uma>mm then // buy condition

compra=1

endif

if (uma-ltp)<=objetivo then

compra=0

endif

if (ltp-umb)>objetivo and umb<mm then // short condition

venta=-1

endif

if (ltp-umb)<=objetivo then

venta=0

endif

Return compra coloured(0,128,0) as "compra", venta coloured(220,20,60) as "venta"

Recomendations

3000 € / $ and max risk of 2% per trade.

Indicators

ExponentialAverage[8](close)

ExponentialAverage[18](close)How it works

Firstly, is a simple trend following system.

Look for a fast price move in whatever direction, this movement must be longer than 45 pips from last touch with Ema8, and then a retracement touching Ema8 will fill our limit order and join the trend.

Fixed Stop ploss and target pprofit give us unreal vision of the strategy in the backtest. However I’ll keep trading it since is profitable for me since March, not as good as backtest results shows, of course… but very interesting… 😉

Why not?

CODE

defparam cumulateorders=false

defparam preloadbars=8

defparam flatbefore=090000

defparam flatafter=213000

mycompra, myventa = CALL "ALEX ATB Indicator"

ema=ExponentialAverage[8](close)

advance=abs(round(ema-ema[1]))

mylot=(((Strategyprofit+3000)*0.02)/30)

if not longonmarket and mycompra=1 then

BuyPrice = ema+advance

buy mylot contract at BuyPrice limit

endif

if not shortonmarket and myventa=-1 then

SellPrice = ema-advance

sellshort mylot contract at sellprice limit

endif

set stop ploss 30

set target pprofit 25

Best trading ever, Adolfo.