Slow Relative Strength Index (Apirine) SRSI

{kind=link}

The Slow Relative Strength Index, SRSI, is a concept made by Vitali Apirine that appear in the TASC (Technical Analysis of Stocks & Commodities) magazine, in April 2015.

This momentum oscillator is derivated from the famous J. Welles Wilder RSI formula. The change of price movements are measured relatively to an exponential moving average movements. The returning values are bounded between 0 and 100.

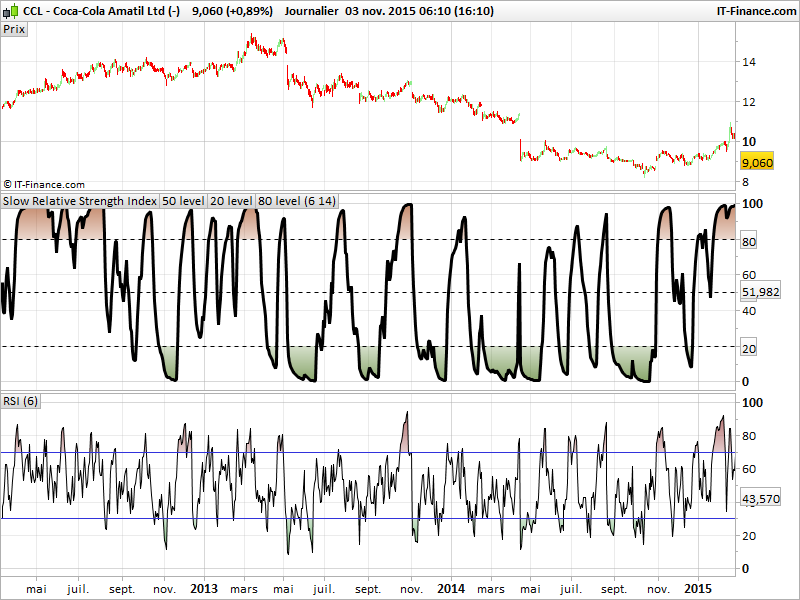

The SRSI can be used for trend following by using its momentum effect but also to detect oversold and overbought zones of price. It tends to be more effective on trending instrument because when price remainin an upper trend, the oscillator remain also in the overbought zone more longer than an original RSI. I attached a screenshot of the original RSI compared the SRSI.

//parameters :

// N = 6

// X = 14

Price = exponentialaverage[X](close)

SF = 1 / N

Change = Price-Price[1]

if barindex <= N+X THEN

NetChgAvg = (Price - Price[N]) / N

TotChgAvg = average[N](ABS(Price-Price[1]))

ELSE

NetChgAvg = NetChgAvg[1] + SF * (Change-NetChgAvg[1])

TotChgAvg = TotChgAvg[1] + SF * (ABS(Change)-TotChgAvg[1])

ENDIF

if TotChgAvg <> 0 THEN

ChgRatio = NetChgAvg / TotChgAvg

ELSE

ChgRatio = 0

ENDIF

SRSI = 50 * (ChgRatio + 1)

RETURN SRSI, 50 as "50 level", 20 as "20 level", 80 as "80 level"

{kind=link}