Standard Error Composite Bands

{kind=link}

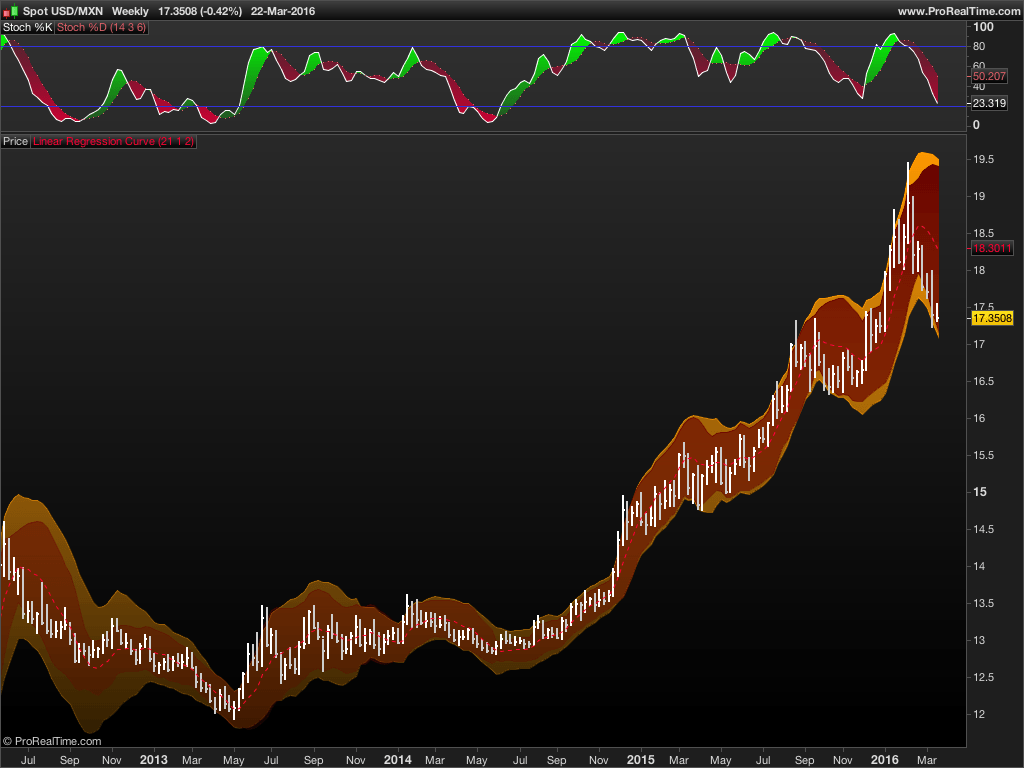

STANDARD ERROR COMPOSITE BANDS

Transcript Code by @XeL_arjona

Ver. 1.00.a

Original implementation idea of bands by: Traders issue: Stocks & Commodities V. 14:9 (375-379):

Standard Error Bands by Jon Andersen

Introduction and Implementation:

STANDARD ERROR BANDS are quite different than Bollinger’s. First, they are bands constructed around a linear regression curve. Second, the bands are based on standard errors with a factor multiplier above and below this regression line. The error bands measure the STANDARD ERROR OF THE ESTIMATE around the linear regression line. Therefore, as a price series follows the course of the regression line the bands will narrow, showing little error in the estimate. As the market gets noisy and random, the error will be greater resulting in wider bands.

An Additional “alpha-beta (y-y’) algorithm” of Standard Error is implemented as additional -Resistance/Support- on bands. The algorithm was originally made for TradingView’s pine version by user @glaz.

Links for further reference:

Standard Error Bands by Jon Andersen Implementation

What is a STANDARD ERROR ? (Wikipedia)

Resumed explanation of what is an STANDARD ERROR OF THE ESTIMATE.

The CODE:

P = 21, SDEG = 1, MF=2

// Standard Error of the Estimate (Composite Bands)

AR = close

N = barindex

LR = Average[SDEG](linearregression[P](AR))

// BETA

bv1 = summation[P](N*AR) - (P*Average[P](N)*Average[P](AR))

bv2 = summation[P](square(N)) - (P*square(Average[P](N)))

CalcB = bv1/bv2

// ALPHA

CalcA = Average[P](AR) - (CalcB*Average[P](N))

// STANDARD ERROR OF THE ESTIMATE

sev1 = Summation[P](square(AR)) - (CalcA*Summation[P](AR)) - (CalcB*Summation[P](N*AR))

sev2 = Summation[P](square(LR-AR))

sev3 = P - 2

SEnarrow = sqrt(sev1/sev3)

SEwide = sqrt(sev2/sev3)

// BANDS

NarrowUB = LR + (SEnarrow*MF)

NarrowBB = LR - (SEnarrow*MF)

WideUB = LR + (SEwide*MF)

WideBB = LR - (SEwide*MF)

// OUTPUT

RETURN LR AS "Linear Regression Curve", NarrowUB AS "StandardError Narrow UpperBand", NarrowBB AS "StandardError Narrow BottmBand", WideUB AS "StandardError Wide UpperBand", WideBB AS "StandardError Wide BottomBand"